The future of Banking is a very hot subject because Banking must successfully face two great challenges …

The first one is:

TACTICAL – How to successfully digitize the operations and services of Banking in this, difficult technologically, transition time.

The second one is:

STRATEGIC – How to successfully face the threat that Banking now can increasingly be done by non-Banking entities.

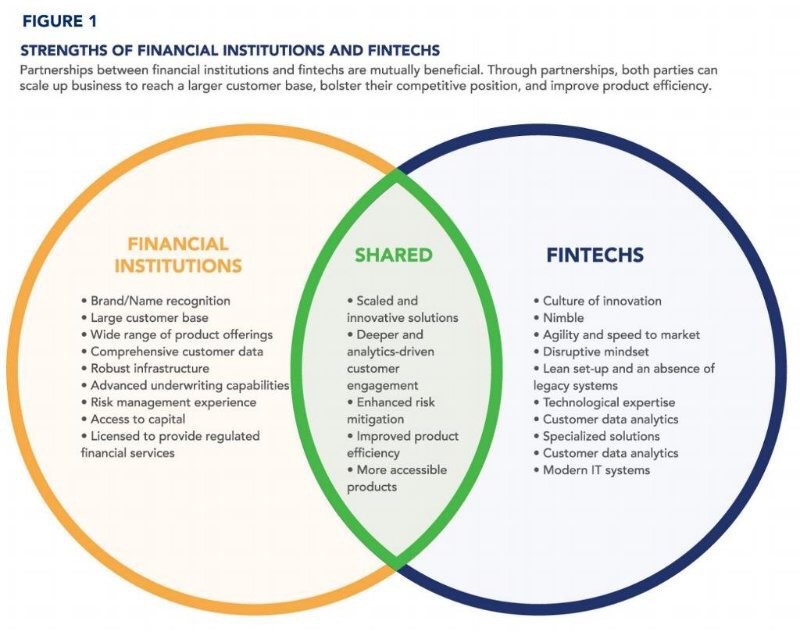

David Jimenez Maireles , who is a brilliant visionary and a rare hybrid of Banking, Fintech and Customer care, among other assets, published this scheme.

If one observes it closely it will be noted that the only strengths of Financial institutions that Fintech Companies do not have are:

- Risk management experience

- Access to Capital

- License to provide regulated Financial Services

- While none of the strengths of Fintech Companies can be found in Financial Institutions.

Although the technical/transactional challenge of Banking digitization and use of revolutionary emerging fintech technology, occupy the attention of the Boards and CEOs of Banks, the strategic challenge is the most threatening one for banks, and it can mainly be properly addressed morally, not digitally.

Eyebrows are already raised. Morality from a Bank? – “Cold like a Banker’s heart” is a favorite expression.

The morality however requested from Banks and Bankers is not philanthropy.

It is Integrity, Trust, Risk understanding and management and the Perception of them by the customers.

The Perception of the above by the Society as a whole and not only the customers, is equally important. Banks must be and perceived to be, that they are trustworthy.

I have been a senior Banker for many years and in spite of my many sins, I cannot be accused of being naive about Banking. So what follows is a reflection on the future of Banking that took me years to understand and formulate.

Banks have suffered greatly in the past decade, but so have their customers. There is a pervading perception that Banks are unsafe, that they neglect their duties in the pursuit of profit, corporate and personal. Whether that is true or not, and in a number of cases it is, the first question of a serious depositor is “can I trust this Bank for the return of my money?”. And only the second question is “can I trust this Bank for the return on my money”.

The depositor is the foundation of Banking.

Unfortunate choices of various Banks worldwide, have already undermined the certainty of trust in Banks in general. Many Banks even big, international ones became also victims of their internal bureaucracy, particularly in procedural and compliance issues. They also suffer from the results of hasty digitization that adopted fintech methods before adapting the procedures to them. They took humans out of the loop prematurely to the detriment of the quality of service.

While this is a extensively spread perception, right or wrong it does not matter, one thing is certain. The next crisis will demolish the Status of Banks and open the way for any other entity that can also provide banking services.

Banks must stop thinking only about the next trimester and digitization, because this strategic threat must be addressed now.

Banking is, or at least should be a service platform, not a pipe industry.

That means two things:

- Trust in the platform

- Technical ability of the platform to perform all Banking functions and transactions and to successfully manage multiple entries and exits.

The Banks focus on the technical side of their Business, especially to reduce costs, not to improve service. They took humans prematurely out of the loop and their customer service level degraded. By assigning serious decision-making to machines, they are on the way to develop employees with Pavlov-like reactions to machine instructions.

This was a Strategic mistake because service degraded and if the customers feel that their Bank does not really care about the level of service that it offers them, the corollary is that Banks only care about their profit and that makes them untrustworthy in the customer’s perception of them. Proof of this displeasure is again provided by the same trustworthy digital/banker/thinker David Jimenez Maireles.

Note that this took place in Sweden, a very advanced digitally Country.

By focusing on the technical side of the Banking Business, Banks, unwillingly gave the opportunity to fintech companies to learn Banking and to be paid for it on top.

Fintech companies can design a banking platform better, than a bank can digitize its banking business by using a fintech company.

In fact, by hastily adopting fintech technologies, Banks taught Banking to the fintech companies at the expense of their customers. The customers suffered all the transition bugs and malfunctions of their fintech applications, which subsequently they perfected to a superior to the Banks level.

If the Banks try to fight fintech companies on the technical field they are bound to lose because in this field they are handicapped. Fintech companies are superior to Banks in this field. How do Banks compete, with a fintech company which operates from a digitized country with digitized currencies, digitized companies, digitized Banking and digitized credit on top of it?

There is however a better field for Banks to fight non-banking intruders and win.

The reason we do business through a Bank is that we trust the Bank to successfully fulfill the undertaking.

Trust and service the keys to the customer relation with a Bank.

Loyalty in a Bank is strong for as long as the values promised are not put in doubt and this depends on maintaining the Trust and the consistency of the quality of service offered, as perceived by the customer.

If therefore the Banks wish to exclude non-Banking intruders from Banking, they must press for stricter not laxer regulation. Certified proof of the institutional suitability of a Bank, in terms of capital adequacy, risk management, transparency and strict internal and external audit procedures must be made stricter.

Only a strict regulatory environment will ensure the uniqueness of the Banking sector and protect it from the intrusion of non-banking institutions.

The requirements for high capital adequacy, proof of competence in risk management, lowering of limits of assets to liabilities ratios, more severe stress tests and certification of the above by stricter internal and external controls, will push some Banks out of business and reduce the profits margins of most Banks.

This, however, is the only way that the Banking sector, institutionally, will survive the assault of non-Banking entities. The customer learns through experience and few banking customers, particularly on the retail side, have an understanding of what constitutes a proper and reasonably safe Bank.

Only the regulator can really protect the customer of a Bank. By protecting the customer, the Bank itself is also protected.

The future of Banking lies in morality. This is a time that the general moral framework of Societies, and particularly that of Governments of Countries, worldwide is fractured.

Examples are rife around the World, where a Country uses the regulated banking system to finance its deficits, through the mandatory state bond purchase, or mandatory financing of systemic industries or state control businesses. It is the case of Germany and Deutsche Bank, or the Italian Banks, the Greek example, even the US Federal Reserve where Policy was that 99% of the home mortgages pass through Freddy Mac and Fanny May, both Government agencies which sell them at the end to the Fed.

Then Countries relax Banking regulations to allow some profitability to the Banks. Then Banks take excessive risks. Then the Countries use the Central Banks to print money to save both Banks and the State.

What happens to the banking system if the client distrusts the Bank and the Country at the same time?

This is all the more reason for Banks to espouse moral standards that will restore the traditional values of Banking.

The technical side of Banking can and will be improved and aligned with the rest of the technological progress. Financial institutions will learn that, as with IT, it is best to develop fintech internally and not subcontract it.

It is only a question of time and money.

Reputation needs much more than time and money.

Money must have a moral center, and with the development of greater responsibility in Banking, greater profit will follow.